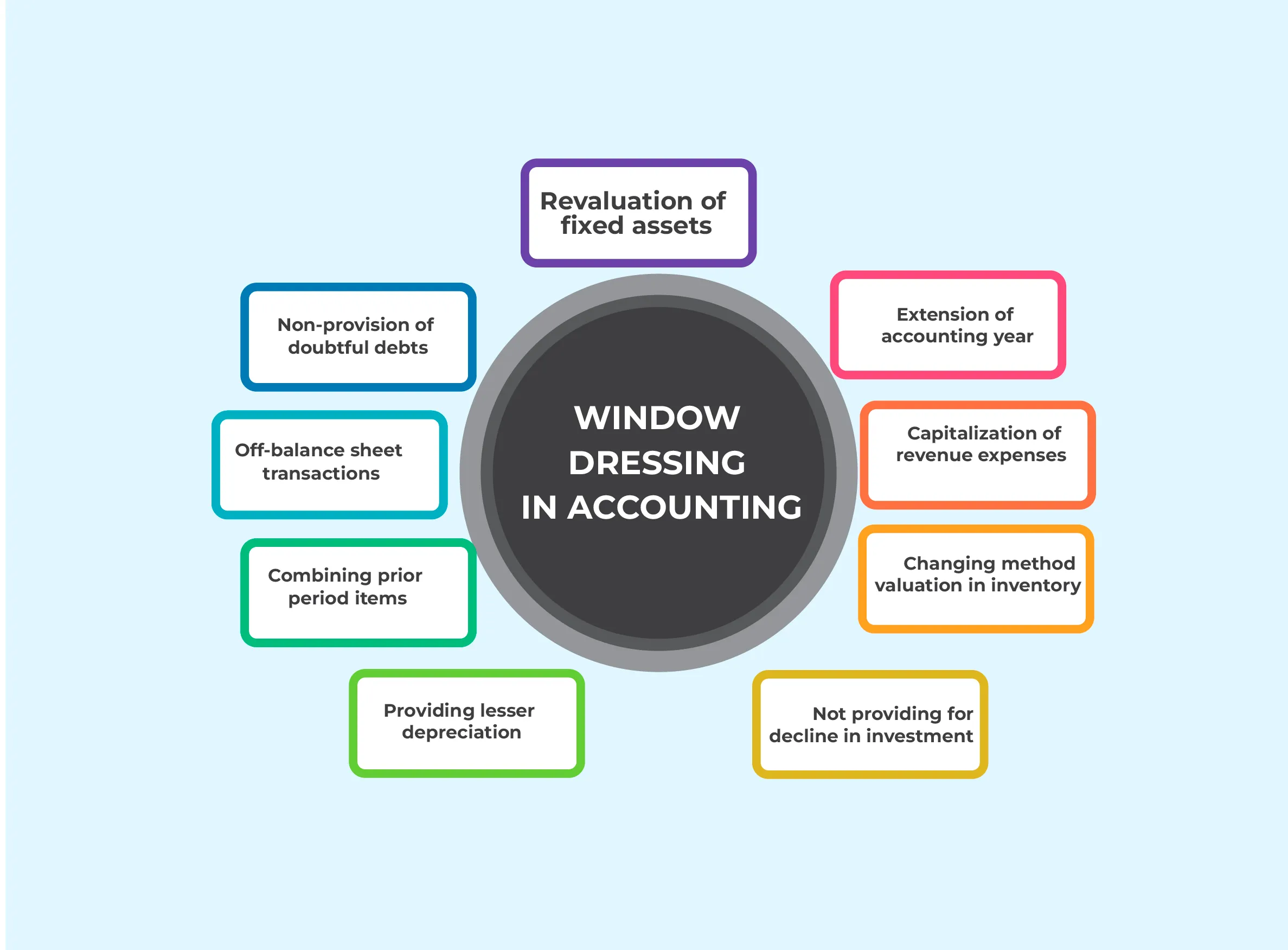

Specifics of Window Dressing

Window dressing is an aggregate term used to denote a number of specific activities. Whitewash, blue wash and green wash are primarily synonyms of window dressing used by NGOs.

- Blue wash, for example, criticizes corporations which associate themselves with the humanitarian community through voluntary association with the United Nations, without provisions for accountability.

- Green wash may be defined as the occurrence of socially and environmentally destructive corporations which attempts to preserve and expand their markets by disguising themselves as friends of the environment and leaders in the struggle to eradicate poverty.

- Whitewash is a compliance procedure under the Corporations Act 2001. Section 260A of the Corporations Act 2001 which essentially permits a company to give any financial assistance to a person to acquire shares in the said company, but only if the giving the financial assistance does not materially prejudice the interests of the company or its shareholders.

Window Dressing Mechanisms

Window dressing in any corporation is done by the two main processes which are as follows-

- Window dressing by the process of sales management

If a corporation has a goal to increase their sales revenue in any segment, one way to do this is to lower the price of goods in that segment. It potentially leads to more booked sales, but eventually with time a lower profit margin, and a depletion of inventories is seen as the abnormal sales volume comes to light.

When firms chose this process, it would imply higher profitability in the non-favorable segment for conglomerates that are classified into favorable industries. Firms increasing sales are observed to be classified into favorable industries as there is very little incentive to change segment sales, which then determine industry classification.

- Window dressing by accounting manipulation

Another alternative solution to companies managing sales to be classified in the groups of favorable industries is that they simply manoevure accounting statements to the similar end. Although this in itself would not singlehandedly explain the inventory and profitability results at the segment level, it is still used as a complementary source which helps to achieve the same goal.

When firms manipulate their sales figures in the accounting statements, this manipulation will later definitely need to be corrected in a future restatement that more accurately shows the firm operations.

The overall manipulation leads to a likelihood of switchers which is larger than other firms, but only marginally significantly so. These firms, in contrast, are proven to more likely restate earnings compared to non switchers.

Now that you know the mechanics of window dressing, contact our round the clock customer service team accessible round the globe who have an unwavering goal to answer all your assignment related problems and provide us an opportunity with your Window Dressing assignment writing help.

3 Bellbridge Dr, Hoppers Crossing, Melbourne VIC 3029

3 Bellbridge Dr, Hoppers Crossing, Melbourne VIC 3029